Digital tax administration systems: A literature review in Scopus (2012-2022)

DOI:

https://doi.org/10.51252/rcsi.v3i2.525Keywords:

big data, blockchain, digitalization, information systemAbstract

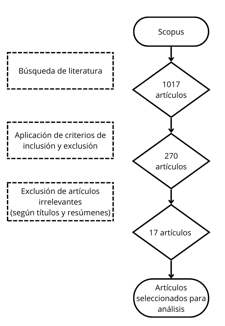

The study analyzed the use of advanced technologies in fiscal and financial management in public institutions, with an emphasis on the implementation of technological tools and the associated challenges. Through a systematic review of 17 scientific articles indexed in Scopus (2012-2022), technologies such as Blockchain, Geographic Information Systems (GIS), Big Data, IoT and neural networks were identified, highlighting their impact on operational efficiency, tax collection and fraud detection. The results reveal that these technologies have improved process automation, decision-making and financial security, while the digitalization of customs and tax processes has optimized data collection and budgeting efficiency. However, challenges persist in terms of technical resources, system interoperability and data security. The success of the implementation of these technologies depends largely on the ability of institutions to modernize their existing systems and adapt to technological advances. In conclusion, emerging technologies offer a considerable opportunity to transform fiscal and financial management in the public sector, although challenges will need to continue to be addressed to maximize their potential impact.

Downloads

References

Al-Mawali, H., Al Natour, A. R., Zaidan, H., Shishan, F., & Rumman, G. A. (2022). Examining the Factors Influencing E-Tax Declaration Usage among Academics’ Taxpayers in Jordan. Informatics, 9(4). https://doi.org/10.3390/informatics9040092

Alanezi, M. A., Mahmood, A. K., & Basri, S. (2012). E-government service quality: A qualitative evaluation in the case of Saudi Arabia. Electronic Journal of Information Systems in Developing Countries, 54(1). https://doi.org/10.1002/j.1681-4835.2012.tb00382.x

Alm, J. (2021). Tax evasion, technology, and inequality. Economics of Governance, 22(4), 321–343. https://doi.org/10.1007/s10101-021-00247-w

Anagnostopoulos, D., Papadopoulos, T., Stamati, T., & Balta, M. E. (2020). Policy and Information Systems Implementation: the Greek Property Tax Information System Case. Information Systems Frontiers, 22(4), 791–802. https://doi.org/10.1007/s10796-018-9887-y

Bassey, E., Mulligan, E., & Ojo, A. (2022). A conceptual framework for digital tax administration - A systematic review. Government Information Quarterly, 39(4), 101754. https://doi.org/10.1016/j.giq.2022.101754

Buldas, A., Draheim, D., Gault, M., Laanoja, R., Nagumo, T., Saarepera, M., Shah, S. A., Simm, J., Steiner, J., Tammet, T., Tammet, T., & Truu, A. (2022). An Ultra-Scalable Blockchain Platform for Universal Asset Tokenization: Design and Implementation. IEEE Access, 10, 77284–77322. https://doi.org/10.1109/ACCESS.2022.3192837

Cronin, P., Ryan, F., & Coughlan, M. (2008). Undertaking a literature review: a step-by-step approach. British Journal of Nursing, 17(1), 38–43. https://doi.org/10.12968/bjon.2008.17.1.28059

Deng, H., & Xie, D. (2021). Application of the Tax Policy in the Free-Trade Zone Based on Big Data and Internet of Things Technology. Mobile Information Systems, 2021. https://doi.org/10.1155/2021/3315160

Eom, S.-J., & Lee, J. (2022). Digital government transformation in turbulent times: Responses, challenges, and future direction. Government Information Quarterly, 39(2), 101690. https://doi.org/10.1016/j.giq.2022.101690

Jiang, Y., Qin, J., & Khan, H. (2022). The Effect of Tax-Collection Mechanism and Management on Enterprise Technological Innovation: Evidence from China. Sustainability, 14(14), 8836. https://doi.org/10.3390/su14148836

Johar, S., Ahmad, N., Asher, W., Cruickshank, H., & Durrani, A. (2021). Research and Applied Perspective to Blockchain Technology: A Comprehensive Survey. Applied Sciences, 11(14), 6252. https://doi.org/10.3390/app11146252

Lutfi, A., Al-Okaily, M., Alsyouf, A., & Alrawad, M. (2022). Evaluating the D&M IS Success Model in the Context of Accounting Information System and Sustainable Decision Making. Sustainability (Switzerland), 14(13). https://doi.org/10.3390/su14138120

Malodia, S., Dhir, A., Mishra, M., & Bhatti, Z. A. (2021). Future of e-Government: An integrated conceptual framework. Technological Forecasting and Social Change, 173, 121102. https://doi.org/10.1016/j.techfore.2021.121102

Mu, R., Fentaw, N. M., & Zhang, L. (2022). The Impacts of Value-Added Tax Audit on Tax Revenue Performance: The Mediating Role of Electronics Tax System, Evidence from the Amhara Region, Ethiopia. Sustainability (Switzerland), 14(10). https://doi.org/10.3390/su14106105

Night, S., & Bananuka, J. (2019). The mediating role of adoption of an electronic tax system in the relationship between attitude towards electronic tax system and tax compliance. Journal of Economics, Finance and Administrative Science, 25(49), 73–88. https://doi.org/10.1108/JEFAS-07-2018-0066

Peláez-Repiso, A., Sánchez-Núñez, P., & García Calvente, Y. (2021). Tax Regulation on Blockchain and Cryptocurrency: The Implications for Open Innovation. Journal of Open Innovation: Technology, Market, and Complexity, 7(1), 98. https://doi.org/10.3390/joitmc7010098

Politou, E., Alepis, E., & Patsakis, C. (2019). Profiling tax and financial behaviour with big data under the GDPR. Computer Law & Security Review, 35(3), 306–329. https://doi.org/10.1016/j.clsr.2019.01.003

Rocha-Salazar, J.-D.-J., Segovia-Vargas, M.-J., & Camacho-Miñano, M.-D.-M. (2022). Detection of shell companies in financial institutions using dynamic social network. Expert Systems with Applications, 207. https://doi.org/10.1016/j.eswa.2022.117981

Serrano, W. (2020). Genetic and deep learning clusters based on neural networks for management decision structures. Neural Computing and Applications, 32(9), 4187–4211. https://doi.org/10.1007/s00521-019-04231-8

Setyowati, M. S., De Utami, N. sila, Saragih, A. H., & Hendrawan, A. (2020). Blockchain Technology Application for Value-Added Tax Systems. Journal of Open Innovation: Technology, Market, and Complexity, 6(4), 156. https://doi.org/10.3390/joitmc6040156

Singh, A., Singh, S. K., Meraj, G., Kanga, S., Farooq, M., Kranjčić, N., Đurin, B., & Sudhanshu. (2022). Designing Geographic Information System Based Property Tax Assessment in India. Smart Cities, 5(1), 364–381. https://doi.org/10.3390/smartcities5010021

Singh, P., Dwivedi, Y. K., Kahlon, K. S., Sawhney, R. S., Alalwan, A. A., & Rana, N. P. (2020). Smart Monitoring and Controlling of Government Policies Using Social Media and Cloud Computing. Information Systems Frontiers, 22(2), 315–337. https://doi.org/10.1007/s10796-019-09916-y

Strauss, H., Fawcett, T., & Schutte, D. (2020). Tax risk assessment and assurance reform in response to the digitalised economy. Journal of Telecommunications and the Digital Economy, 8(4), 96–126. https://doi.org/10.18080/JTDE.V8N4.306

Umbach, G., & Tkalec, I. (2022). Evaluating e-governance through e-government: Practices and challenges of assessing the digitalisation of public governmental services. Evaluation and Program Planning, 93, 102118. https://doi.org/10.1016/j.evalprogplan.2022.102118

Uyar, A., Nimer, K., Kuzey, C., Shahbaz, M., & Schneider, F. (2021). Can e-government initiatives alleviate tax evasion? The moderation effect of ICT. Technological Forecasting and Social Change, 166, 120597. https://doi.org/10.1016/j.techfore.2021.120597

Vysochan, O., Vysochan, O., Yasinska, A., & Hyk, V. (2021). Selection of Accounting Software for Small and Medium Enterprises Using the Fuzzy Topsis Method. TEM Journal, 10(3), 1348–1356. https://doi.org/10.18421/TEM103-43

Wu, Q., Xu, X., & Lin, R. (2021). Government incentive mechanism of closed-loop supply chain based on information asymmetry. RAIRO - Operations Research, 55(6), 3359–3378. https://doi.org/10.1051/ro/2021124

Xiao, F., Chen, R.-S., Zhang, W., Chen, Y.-C., Lu, S.-Y., Chen, Y.-Q., Xiong, N., & Chen, C.-M. (2019). Design and Analysis of a Strengthen Internal Control Scheme for Smart Trust Financial Service. IEEE Access, 7, 163202–163218. https://doi.org/10.1109/ACCESS.2019.2945056

Zasko, V., Sidorova, E., Komarova, V., Boboshko, D., & Dontsova, O. (2021). Digitization of the customs revenue administration as a factor of the enhancement of the budget efficiency of the russian federation. Sustainability (Switzerland), 13(19). https://doi.org/10.3390/su131910757

Zhang, W., Chen, R.-S., Chen, Y.-C., Lu, S.-Y., Xiong, N., & Chen, C.-M. (2019). An Effective Digital System for Intelligent Financial Environments. IEEE Access, 7, 155965–155976. https://doi.org/10.1109/ACCESS.2019.2943907

Downloads

Published

How to Cite

Issue

Section

License

Copyright (c) 2023 Jonatan Jesus Cardenas-López

This work is licensed under a Creative Commons Attribution 4.0 International License.

The authors retain their rights:

a. The authors retain their trademark and patent rights, as well as any process or procedure described in the article.

b. The authors retain the right to share, copy, distribute, execute and publicly communicate the article published in the Revista Científica de Sistemas e Informática (RCSI) (for example, place it in an institutional repository or publish it in a book), with an acknowledgment of its initial publication in the RCSI.

c. Authors retain the right to make a subsequent publication of their work, to use the article or any part of it (for example: a compilation of their works, notes for conferences, thesis, or for a book), provided that they indicate the source of publication (authors of the work, journal, volume, number and date).